Your contact

Dimitri M. Rotter

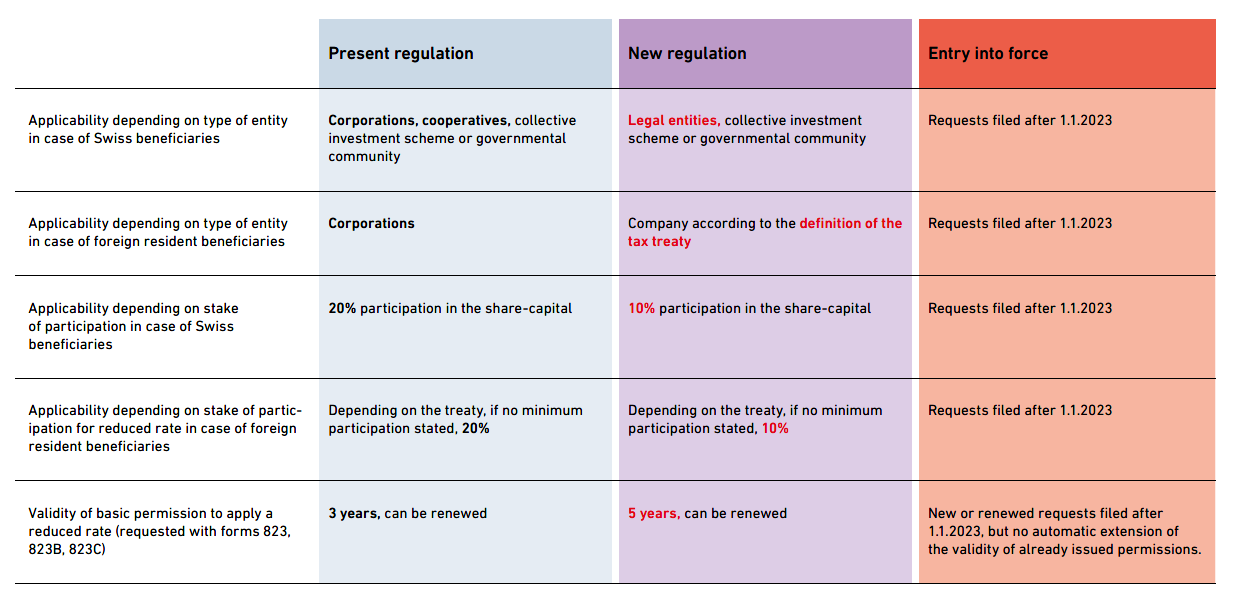

On 4 May 2022, the Federal Council has amended the ordinance on Swiss withholding tax and broadened the application of the notification procedure.

In certain cases where withholding tax can be refunded, it is possible instead of paying the withholding tax and refunding it, to only notify this to the tax administration (“Meldeverfahren”).

The notification procedure applies inter alia in case of full refund of the Swiss withholding tax by Swiss parent companies and in case of applicability of the lower tax treaty rate for qualifying participations of parent companies being resident abroad. The hurdles for the applicability of the notification procedure have been lowered by the bespoken amendment, as reflected in the below table:

(click on the table to enlarge)

The following improvements have not been implemented:

- Complete abolition of the notification procedure if the conditions for a reduction of the withholding tax to zero percent are fulfilled.

- Applicability of the notification procedure for any kind of dividends within a group of companies:

As the participation in consolidated subsidiaries will always be more than 10%, there is no issue for true dividends distributed to the parent company, the issue is for deemed dividends based on benefits in kind to other group companies. Deemed dividends to the direct parent company do basically benefit from the notification procedure. However, for deemed dividends to indirect parent companies (grandmother company) or sister companies an application of the notification procedure would also be welcome as they are basically entitled to full or partial refund of the Swiss withholding tax. However for these beneficiaries presently the notification procedure is only available in the very limited case of a correction in the course of a formal tax audit (art. 24 para 1 lit. a of the ordinance). The notes of the tax administration accompanying the amendment state that this issue was analyzed but rejected.

It is however unclear whether the law itself (i.e. not the ordinance) does not explicitly foresee the application of the notification procedure also in such cases (art. 20 para 2 sentence 2of the withholding tax act), independently from the ordinance, and as a formal law supersedes the ordinance. Certain authors are of the opinion that this is the case (see Stefan Oesterhelt and Susanne Schreiber in Expert Focus 2020, issue 12, pages 978 ff.).

For any further details, please feel free to reach out to our tax team.